Industrial Revolutionary

How artificial intelligence will fuel Canadian productivity and prosperityThe future of driving has become a fact of daily life in Austin, Texas, my seasonal home. Waymo’s robotaxis, with passengers but no drivers, are ubiquitous — smoothly gliding around the busiest downtown streets; squeezing into crowded parking lots; and stopping obediently for careless pedestrians. The sight of a steering wheel with no one behind it turning left in front of you is, frankly, spooky but we’re already getting used to it; the same way we’ve gotten used to digital “assistants” popping up to answer our questions when we try to book a flight or cancel our cable.

Robotaxis and chatbots are early harbingers of a revolutionary artificial intelligence (AI) that is destined to transform economies and cultures — and in fact just about everything. AI amplifies, and sometimes replaces, the capability of the human mind to process and act on the information conveyed by our senses. This is made possible by combining the mind-boggling power of the latest computer hardware with awesome feats of software engineering that have harnessed that power. The result is AIs that can “learn” to function in unstructured and uncertain environments, whether it’s navigating busy streets, identifying a worrisome abnormality in an X-ray, providing precise advance warning of extreme weather events or conjuring up in seconds a draft multimedia funding pitch for your latest great idea. The list goes on and we’re just getting started.

While the precise trajectory of AI is impossible to foresee, it’s certain there’s no going back because:

- AI’s potential benefits are incredibly compelling;

- The world cannot un-learn AI, and global competition among businesses will continue to drive the technology;

- It’s a borderless technology that will become increasingly available to anyone, anywhere; and

- The major players (U.S., China, EU) see their economic prosperity and military security at stake and thus find themselves in an AI race without a finish line.

The potential power of AI and the uncertainty surrounding the course of its development have understandably caused widespread anxiety. Particularly in Canada and other advanced economies, the public discussion has focused far more on the potential risks of AI than on the enormous benefits it holds in store. The objective of this paper is to explore those benefits while also suggesting how certain foreseeable risks can be overcome.

Fundamentally, the paper makes the positive case for AI as a “general purpose technology” — analogous in impact to previous world-changing technologies like the steam engine, electrification and the microchip — that promises to reinvigorate economic growth through sustained impact on productivity globally. The paper also serves as a scene-setter for subsequent reports by the Public Policy Forum that will identify specific opportunities and challenges leading to policy recommendations to enable Canada to maximize the net benefit of the AI revolution.

We begin by explaining why productivity and economic growth in Canada and other highly developed economies have been gradually declining for decades and how the advent of powerful artificial intelligence will eventually reverse the trend. The discussion then turns to the need to manage three risks — AI’s impact on jobs, competition and product regulation — that could delay or seriously mitigate its benefit. The paper concludes with a high-level assessment of Canada’s readiness to participate in and benefit from the AI revolution. While it is outside the scope of this paper to make new policy recommendations, three theme areas are proposed to support an AI industrial strategy for Canada.

By now, it’s well known that the growth rate of Canada’s GDP per capita has been in a deep funk — the per person output of the economy is now barely greater than it was a decade ago.[1] Average living standards march in step with GDP per capita. Although this is not a perfect measure and does not adequately capture quality of life, GDP correlates positively, across nations and regions, with a great many social indicators, including life expectancy, health status and the incidence and consequences of poverty. Moreover, GDP defines the tax base and is therefore the ultimate source of funds for the social and other purposes of government. When the growth rate of per capita GDP declines, both average incomes and government resources are pinched. The sense of national opportunity can fade and the public temper can sour.

What is less well-known or appreciated is that this recent decline is not a new phenomenon. The rate of growth of Canada’s per capita GDP has been decreasing for many decades (see Figure 1). In fact, a similar trend[2] is seen in virtually all highly developed economies, the U.S. included. The robust economic growth rates of the post-war period seem a thing of the past, and the rising prosperity once taken for granted seems now impossible to achieve.

Figure 1

Source: Centre for the Study of Living Standards data base and author’s calculations.

A primary objective of this paper is to explain why this has occurred and describe how the application of artificial intelligence throughout the global economy promises to reverse the trend.

Just why has per capita economic growth been in a long decline in virtually all highly developed countries? The most important reason is that the rate of growth of productivity — the amount of GDP generated per hour of work, averaged across the economy — has been falling amid the ups and downs of the business cycle for most of the past 75 years.[3] If short-run fluctuations are averaged out to focus on the trend (see Figure 2), productivity in Canada, the U.S., and western Europe grew at about four percent in the immediate aftermath of the Second World War. The steady decline thereafter was interrupted only by a decade of rising productivity growth in the U.S. and Canada in the 1990s driven by the application to business processes of computer and communications technology. Unfortunately, that mini boom was not sustained and the rate of productivity growth throughout the West resumed its weakening trend. The pervasiveness of this phenomenon, both over time and across very different political systems, implies that the causes are deeply systemic. They have little to do with the political blame-shifting that dominates the news cycle and cannot be resolved by silver-bullet policy remedies.

Weak productivity has not been the only factor weighing on per capita GDP. The number of workers as a share of the population (the employment ratio) also matters. For the last several decades, the growth of that ratio slowed as women became more fully integrated into the paid workforce and the labour force participation rate plateaued. Meanwhile, the populations in advanced economies have been growing older as both birth rates and death rates declined, which also causes the growth of the employment ratio to fall, intensifying the drag on the growth rate of per capita GDP.

Figure 2

Source: The long-term productivity data base, which is maintained by Bergeaud, A., Cette, G. and Lecat, R. The graph was plotted by P. Nicholson using data taken directly from the data base.

Nevertheless, productivity growth is the most important factor going forward and it has faced several structural headwinds:

- The increasing role in the economy of services which now constitute about 80 percent of GDP and is less amenable to the productivity-boosting effect of traditional automation and mass production than has been the case for goods production, particularly manufacturing;

- The declining growth impetus from human capital as average educational attainment, at both the secondary and post-secondary levels, plateaued;

- The cumulative effect of regulation: While often justified to mitigate market failures and to achieve social and environmental objectives, a dense web of regulations has increasingly constrained decisions directed solely to growth maximization; and

- Diminishing returns from the group of technologies that have powered productivity growth for more than a century, such as the electric motor, factory automation, industrial chemistry, the internal combustion engine and telecommunications.[4]

Take cars or passenger aircraft or even the internet. Each steadily got better and became more widely adopted for many years until technical improvement plateaued and their adoption rate saturated. This “S-curve” — a slow beginning followed by a period of rapid improvement before eventually tapering off — is characteristic of every technological innovation and is mirrored by a second S-curve of diffusion from early adopters to the majority in the middle and finally to the stubborn holdouts. This process of innovation and diffusion is the fundamental engine of productivity and economic growth.

Simple arithmetic explains why the productivity growth impetus of every specific innovation eventually declines. It’s because sustaining an exponential growth rate — i.e. a constant percentage increase each year — becomes more and more challenging. The arithmetic of compounding means that the required absolute annual increment of growth keeps increasing while the returns on any specific technological innovation inevitably diminish. Fresh innovation is the only way to increase, or even sustain, a constant growth rate.[5]

Economic history demonstrates the extraordinary role in growth played by certain technologies that have pervasive effects on a very broad range of activities — for example, the steam engine, electricity and the microchip, among others. Dubbed general purpose technologies[6] (GPTs), they powered successive industrial revolutions by underpinning dense webs of complementary innovations in transportation, novel materials, construction, factory automation, retailing and on and on. Every GPT is an innovation amplifier that stimulates a great deal more innovation and thus boosts the rate of growth of productivity. Collectively, these GPTs have created the modern world.

For a time, it was believed that applications of the microchip would power a plethora of innovations that would reignite productivity growth. Indeed, by the mid-1990s, the production of information technology and communications (ITC) goods and the application of computers to business processes caused a productivity boom, but it lasted[7] only through the early 2000s. The above-noted structural headwinds proved to be more powerful than the ITC-driven productivity surge. Stronger medicine is needed.

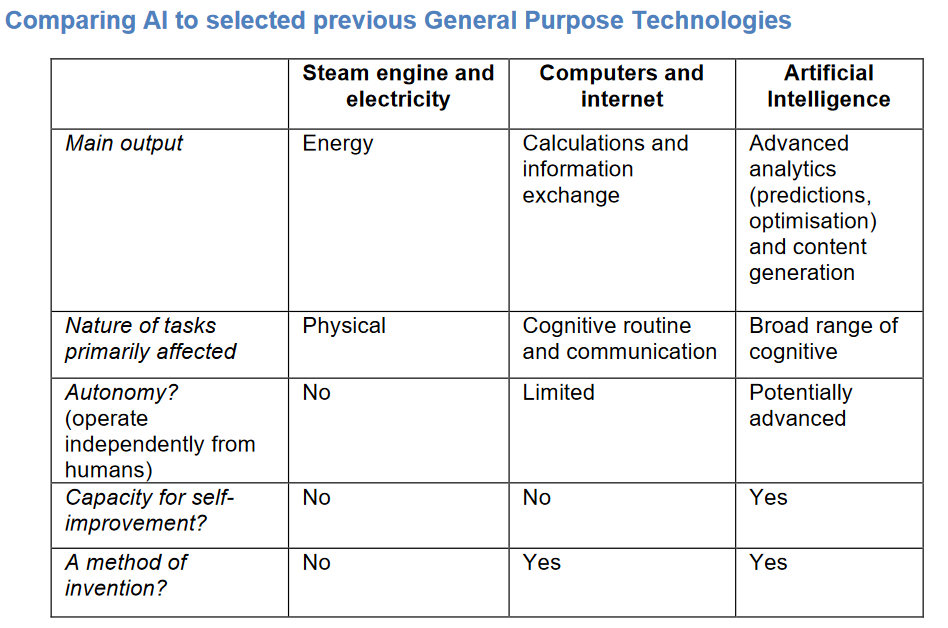

Artificial intelligence is the only technology, existing or on the horizon, with the potential to reverse the decades-long decline in the rate of productivity growth. The potentially unprecedented power of AI derives from its open-ended capacity to amplify and augment the human mind. This sets it utterly apart from any of the transformative technologies of the past (see Figure 3). Fundamentally, AI increases labour productivity by:

- Augmenting human capabilities, thus enabling individuals to create value more quickly; and/or

- Substituting for humans in various tasks, thus creating value without requiring worker hours directly while freeing workers to create value in other ways.

Augmentation typically involves an AI taking on some of the tasks involved in an existing job — often the more routine ones or those that can take advantage of the AI’s information processing speed (see examples below). In such cases, the AI functions as a subordinate co-worker.

In cases of substitution, the AI may be sufficiently sophisticated to replace an existing job entirely — such as a routine customer service respondent — with the worker then freed up to perform some other job. In this case, total output is increased — AI replaces at least the worker’s original output while the replaced worker, if re-employed, produces new additional output — but with usually no net increase in human hours worked. Thus, labour productivity overall increases.[8] Whether AI functions as a co-worker or a substitute will obviously depend on the nature of the job/task and the sophistication of the AI itself. The distinction is familiar from the history of technology and automation; AI is simply the latest manifestation, but now with unprecedented capacities.

What is revolutionary this time is the ability of trained AIs to observe, process and analyze digitally encoded information in all modalities — text, image, sound and even, via sensors, physical touch (see Box I). Moreover, they can do this in unstructured environments and then generate appropriate responses via familiar interfaces with humans. Previous automatons, such as assembly robots in car factories, were programmed to function in highly constrained and predictable environments, much like the early AIs that played a good game of chess but never had the “creativity” to beat the world’s top players. Today’s “generative AIs”[9] are able through training to develop an internal model of some significant aspect of the real-world environment, such as human language, that’s rich enough to infer elements of that environment that were not explicitly present in the training data. That allows such AIs to cope flexibly with novel stimuli and to generate appropriate responses, a capability that is entirely unprecedented.

Figure 3

Source: OECD. The graphic is from Page 12.

That said, today’s most advanced AIs are still far from infallible: they sometimes confidently assert things that are not true (“hallucinate”); they express biases implicit in their training data; they fail at certain tasks that humans can accomplish without even thinking. But they keep improving[10] with better internal software, more powerful hardware and better training data. Fundamental limits may exist, but they’re not yet in sight. Moreover, an AI does not have to be perfect; it only needs to perform reliably better than a human or other alternative in any given situation.

Peeking under the hood of AI

Machine intelligence of a kind has a long history of commercial application —for example, the Jacquard loom, an early 19th-century programmable weaving machine that uses punched cards to control the weaving process, and in the progressive automation of manufacturing ever since. What is so very different today is the phenomenal power of computer technology to enable artificial simulation[11] of behaviour that is increasingly indistinguishable from its human counterpart.

For example, today’s graphic processing units (GPUs), the workhorse of ChatGPT and other generative AIs, perform[12] an unimaginable 300 trillion basic arithmetic operations per second. To put this in perspective, the GPU can do in one second what it would take a human — tapping in one number per second on a keyboard — 10 million years! Such processing power is necessary but still not sufficient to perform the magic of today’s leading-edge AIs. First, data — whether text, image, sound or virtually any other kind — must be digitally encoded into mathematical objects on which GPUs can operate. Then algorithmic procedures need to be designed that enable the AI to “learn” a model of a particular target domain like natural language (the training phase), after which it’s able to compute and regurgitate responses to queries relevant to that domain, whether it’s human language (in the case of Large Language Models, or LLMs, like GPT-4), or images (in the case of “diffusion models” like DALL-E), and so forth.

Today’s leading-edge AIs employ a computational architecture called a “deep neural network”[13] — based loosely on a highly simplified model of the brain — that processes digitally encoded input data via a series of computational parameters that number between 500 billion to more than one trillion in the latest models. By comparison, the human brain contains fewer than 100 billion neurons, although the interconnections among them are vastly more complex than those in contemporary artificial neural networks. On the other hand, artificial networks process information at incomparably greater speed. During the training process, the billions of parameters of the network are tuned, via a mathematical process of error minimization, until the network can form a good internal representation of the training data. Despite the phenomenal processing speed of GPUs, training the latest LLMs still requires two to three months and approximately three trillion-trillion (3 x 1024) individual computations, a number that is vastly beyond human comprehension.

Such brute force is still not enough to “solve” a domain as complex as human language. That depended on an innovation, dubbed the transformer,[14] developed by a team at Google in 2017. The transformer — the “T” in GPT (generative pre-trained transformer) — is a computational architecture that enables LLMs and other leading AIs to recognize subtle contextual features of input data and to do so in a way that scales very efficiently to larger and larger models. As a result, AIs evolved from being expert at identifying and classifying objects of all kinds to being able to generate original content in text, image and sound.

ChatGPT was born in late 2022 and attracted a million global users within five days. The public mind became fixated; both fascinated and alarmed by what seemed to be not just an artificial intelligence but actually an “alien” intelligence. Although computer scientists designed the software that animates today’s leading-edge AIs, and in that sense understand them, no one can see inside the “black box” to follow the countless billions of computational steps from input to output. Sheer complexity can cause surprising and creative behaviour to emerge, as anyone who interacts with a chatbot or image generator soon discovers.[15]

But the lack of transparency as to the step-by-step “reasoning” processes of a generative AI can stand in the way of trusting the output in respect to important decisions, like in medical diagnosis or conducting financial transactions. Lacking transparency as to process, trust can only be established through repeated testing under a range of real-world circumstances, as has occurred, for example, with self-driving vehicles (see Box II).

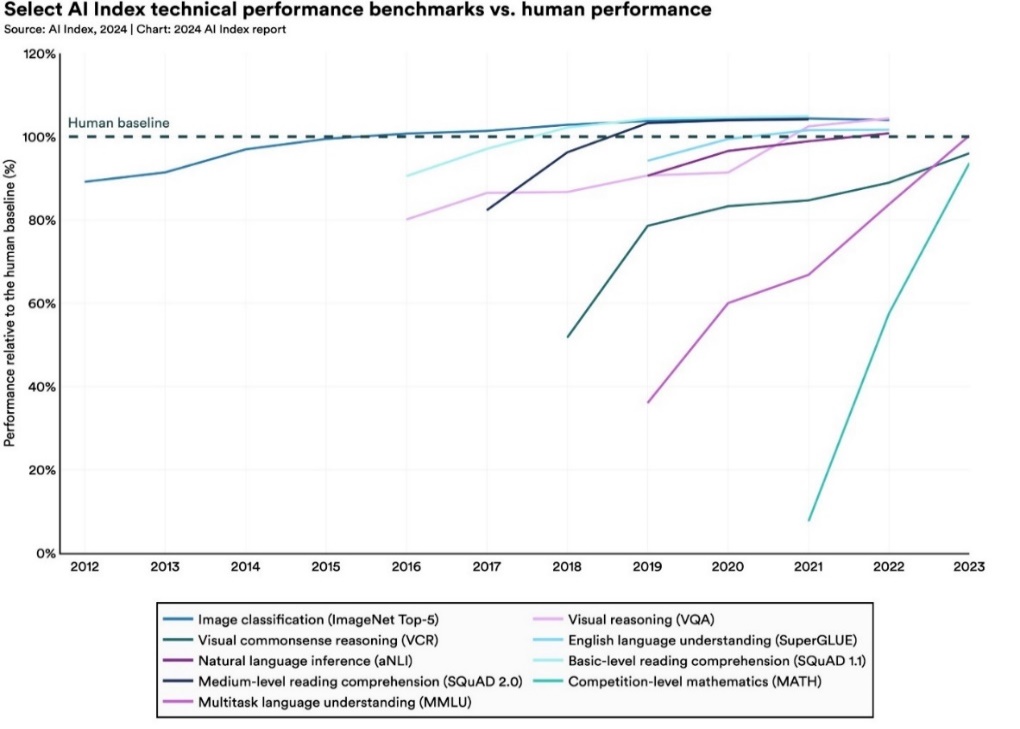

Today, the ability of generative AIs to match or exceed human capability on an ever-expanding range of tasks has increased in rough proportion to the computational power being invested (see Figure 4). At present, the performance limits, if there are any, appear to be related to the availability of much greater volumes of high-quality training data specific to various application areas. Although fundamental conceptual or technological roadblocks may eventually emerge to stymie progress, to date AIs keep exceeding what was thought to be possible and there is no compelling evidence that such advances cannot continue.

Significant electrical energy is required to train and operate today’s “foundation models” like the GPT series. Training such a model is estimated[16] to require roughly 2,000 megawatt hours, or enough to power about 180 Canadian homes for a year. The expansion of AI at very large scale will eventually require new electrical generation capacity,[17] but that will not be a show-stopper. Meanwhile, the much-publicized problems with the first generation of LLMs — the occasional nonsense answers, biases in training data and a relatively weak ability to cope with logical reasoning problems and even simple arithmetic — are being overcome.[18]

While AIs may now be super-human when it comes to passing college exams and conjuring up amazing feats of original text and image generation, the monumental private investment[19] in their development — totaling about US$90 billion globally in 2023, of which $25 billion was allocated to generative AI — will not continue indefinitely without a commensurate financial return.[20] That will depend on developing applications that can be trusted to outperform existing methods in terms of both cost and reliability. Although many AIs, using earlier generations of technology, already meet that test on relatively simple tasks, there are still few widely deployed use cases that exploit the full power of the latest generative models. Today, the really big money makers in the AI ecosystem are the infrastructure giants that supply the powerful computer chips and the “hyperscalers” like Amazon, Google, Microsoft and Meta that provide the cloud resources on which everything rides. Now, having built it, the applications will come.

Figure 4

Source: The graph is taken directly from Chapter 2 of the 2024 AI Index Report.

How AI will drive productivity growth

It’s difficult to predict where AI will have its greatest impact, but several significant use cases are already being implemented or appear to be on the near horizon. With anticipated improvement and increasingly broad adoption, each has the potential to generate significant productivity growth.[21] The examples include:

- Processing data and information of virtually any kind. This is a generic capability from which applications abound in: summarizing enormous volumes of text; pattern recognition to enhance medical diagnosis; and text, image and sound creation in virtually any field, including the creative arts. The AIs are typically co-workers here, amplifying the productivity and creativity of their human superiors.

- Augmenting the productivity of software engineers by significantly increasing output volume without sacrificing quality. The observed improvement[22] has typically been greater for weaker performers. Boosting software productivity and quality has the knock-on effect of improving productivity in virtually every other application area — an AI multiplier effect.

- Boosting productivity in manufacturing[23] and in goods production generally — such as more flexible and intelligent robots, supply chain optimization, better fault detection that leads to proactive maintenance and reduced downtime, generation of design options that optimize manufacturability, regulatory compliance, and cost.

- Improving marketing strategies,[24] for example preparation of promotional materials (text, image, video) or micro-targeted customer identification and inducements. Such applications, while often controversial, underlie the business models of social media platforms and appear to be the most commercially valuable AI applications to date. Indirectly, they provide funding for the development of the leading-edge AI systems by Amazon, Microsoft, Alphabet and Meta.

- Enabling widespread, high-quality language translation[25] implemented in real time with voice synthesis (including via a smart phone app), thereby enhancing productive collaboration and cross-cultural understanding in many everyday situations. Soon every tourist will be multilingual.

- Improved services and capabilities in the financial sector,[26] for example risk analysis, complex document processing associated with lending agreements and regulatory compliance, implementing high-frequency trading strategies and mass personalization of retail financial products.

- Enriching and personalizing education[27] from the early years through adult learning and job training. The potential payoff in terms of productivity will be to build human capital far more efficiently than ever before, including re-training/upskilling workers that AI augments or replaces.

- Boosting productivity across the health-care system[28] to: automate much of the administrative burden using AI to process and provide management recommendations based on information in a variety of formats; assist diagnosis and suggest treatment options; and provide deep analytical support for health system planning to optimize the allocation of scarce resources. Because health care is such a large and growing sector there are few, if any, areas with as much potential for AI-generated productivity growth. Of course, AI solutions will have to be thoroughly tested and proven in practice before wide acceptance and adoption.

- Improving the quality and efficiency of government services.[29] Because most government activity is information-intensive — such as processing payments/receipts that are subject to increasingly complex legal and policy criteria (like tax collection and EI payments), application of regulations, and design of policy solutions — there are a great many tasks ideally suited for AI-based innovation. The potential for significant economy-wide productivity improvement is directly amplified by the sheer scale of modern government, and indirectly by the potential for more effective design and targeting of policy and regulation.

- Equipping various kinds of robots with the capability to perform flexibly[30] in unstructured environments. Self-drive vehicles and applications of drones already demonstrate AIs with agency in the physical world (see Box II).

- Amplifying innovation[31] itself. AI has literally a super-human capacity to: absorb, process, summarize and interpret information of all kinds, including from sensors in the physical environment and from the entirety of the world’s research literature; recognize subtle patterns in unstructured data, including insights that cross conventional disciplinary boundaries; perform increasingly complex logical inference (until recently this was a major weakness of LLMs); and generate hypotheses based on all of the foregoing and engage in dialog with human researchers. These capacities to augment human research skills have the potential to radically increase the productivity of the discovery process itself. This will ultimately be the most transformative impact of AI since it promises to increase the rate of productivity growth of the economy as a whole.

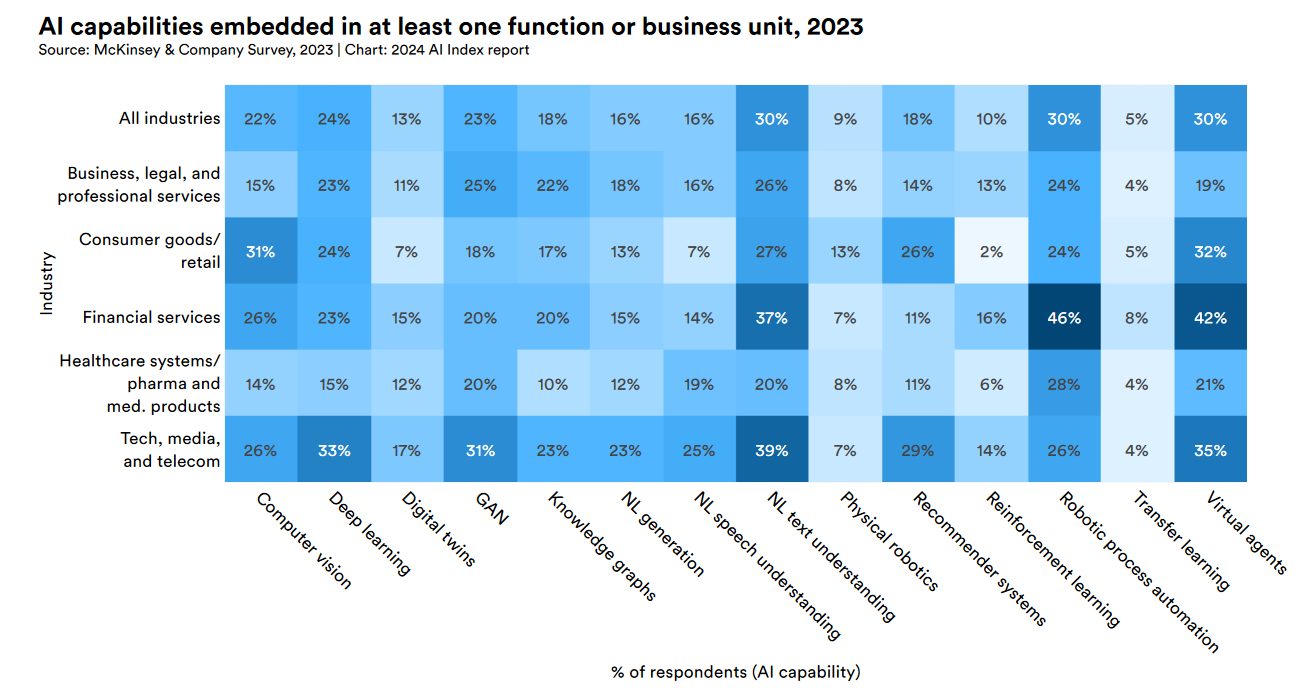

The following table (see Figure 5), based on data from McKinsey & Co., illustrates the uptake of various AI capabilities across a range of sectors. Although still early days, it’s already evident that AI has the salient characteristics of a GPT with the potential to accelerate productivity across much of the economy. In particular, AI promises to have a revolutionary impact on productivity in services, much as earlier generations of technology had in goods production, notably in agriculture and manufacturing.

Figure 5

Source: The figure is taken directly from page 48 of the 2024 AI Index Report. The original data is from McKinsey & Co as cited on the graphic.

The hallmark of contemporary AI is the ability to function in relatively unstructured environments with the flexibility to respond to the unexpected (see Box II). For an AI to be effective in specific application areas, in addition to generic capability it needs to be specifically tailored — for example, trained on high-quality data relevant to the application area. This will increase the efficiency and especially the reliability essential to building the trust required for mission-critical applications and profitable business models. While artificial intelligence that is equal or superior to human intelligence in every respect — referred to as artificial general intelligence[32] or AGI — may someday be achieved, what seems most likely in the near- to mid-term is the evolution of specialized AI “modules” optimized for specific domains.

Autonomous vehicles — AIs as agents in the physical world

As of late 2024, the Google spin-off company Waymo is carrying more than 100,000 riders[33] a week in its fleet of wholly autonomous taxis — with no driver at all — along the downtown streets of San Francisco, Phoenix, Austin and Los Angeles. Once seen as a threat to public safety, they’ve proven so safe and reliable that residents rarely give them a second glance. Waymo’s amazing achievement is the culmination of more than 35 million kilometres of on-road training dating from 2015. The driverless vehicles need to operate safely in an unpredictable urban roadway environment, drawing on sensor data that creates a picture of that environment as it evolves in real time. The next technical step, now underway, is to be authorized to operate on freeways, where speeds create an even higher bar for safety and rapid response. Yet the biggest challenge ahead is to turn Waymo’s miraculous technology into a viable business, a goal that is still on the horizon.

Waymo is simply the farthest along among a great many startups[34] in the field. Some, like Tesla and the U.K. company Wayve, have focused on advanced driver-assistance technology. Others — notably the Canadian startup Waabi[35] — have targeted long-haul trucking. Meanwhile, at the leading edge of the technology, Waabi, Waymo and a few others seek to combine the transformer architecture[36] employed by LLMs with the standard sensors and AI software that already operate autonomous vehicles. The idea is to train the autonomous system to be even more adept at predicting the real-time behaviour of objects in the driving environment, much as LLMs can predict the most appropriate next word in a text response.

The autonomous vehicle is essentially a new species of AI operating as an intelligent agent in the physical world. This represents a significant step beyond large language models because, apart from what is implicitly encoded in an LLM’s training data, those models have no understanding of how the physical world works and thus lack “common sense.” This compromises the ability of such models to resolve certain ambiguities that are intuitive to humans.

For example, if we are told that “the gift could not fit in the suitcase because it was too big,” we immediately understand that it is the gift, and not the suitcase, that is too big. An AI trained just on word patterns may not be able to make that inference. The self-drive vehicle, on the other hand, is out in the physical world, processing and acting on real-time information streamed from multiple sensors. By adding a transformer element, analogous to what has given the LLM its uncanny ability to understand text, autonomous vehicles may eventually develop an equally uncanny ability to “understand” how the physical world works. In this way, self-drive cars, drones and mobile robots of various kinds will learn about the tangible world from direct experience, much as human infants do. The implications for productivity, and much else, are profound.

There have been a number of attempts to estimate[37] the increment of productivity and GDP growth that can be expected from AI applications that are either in place or reasonably foreseeable.

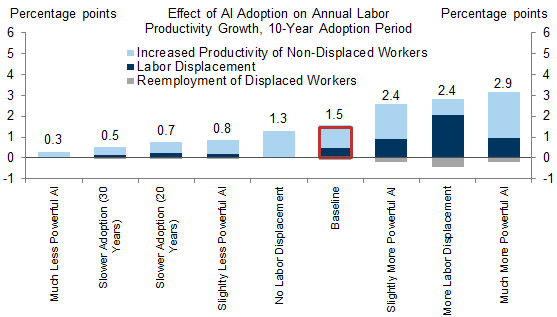

Goldman Sachs, in a widely cited analysis[38] in 2023, projected AI would cause the rate of growth of U.S. productivity to increase by an annual average of almost 1.5 percentage points over a 10-year period following widespread adoption of AI applications. That may seem a small number, but it represents a more than doubling of the current trend rate, with much greater increases in sectors where AI applications show the earliest potential. The projection (see Figure 6) was subject to large uncertainty — ranging from a minimal increase of 0.3 percentage points to a transformative 2.9 points — depending on the difficulty of the tasks AI will be able to perform and the number of jobs that would be affected.

Figure 6

Source: The graphic is Exhibit 13 in this document.

A recent analysis by TD Economics estimated[39] that ramping up AI adoption could raise Canada’s GDP by five to eight percent in 10 years relative to its baseline projection. This would translate to an AI-induced increase in the rate of productivity growth of 0.5-0.7 percentage points. While that is at the lower end of projections by Goldman Sachs and most international projections, it’s still significant by comparison with the dismal growth rate of Canada’s productivity in recent years. And the possibility exists for a much larger productivity boost if the pace and breadth of AI adoption by Canadian businesses exceeds the assumptions in the TD projection.

Along with the optimists, there are also some well-informed skeptics, notably respected MIT economics professor Daron Acemoglu, who in a June 2024 commentary[40] concluded: “Given the focus and architecture of generative AI technology today, truly transformative changes won’t happen quickly and few if any will likely occur within the next 10 years. The largest impacts of the technology in the coming years will most likely revolve around pure mental tasks, which are non-trivial in number and size, but not huge.” Acemoglu is nevertheless optimistic that generative AI “has the potential to fundamentally change the process of scientific discovery.” His skepticism relates primarily to timing.

Bank of Canada governor Tiff Macklem expressed similar sentiments in a September 2024 speech:[41] “In the long run, we can expect AI to boost productivity… AI has all the hallmarks of a general purpose technology, or GPT. But how large and how wide-ranging are hard to predict. We know from history that it takes years for a GPT to diffuse through the economy. We also know that the first applications are typically less transformative than the new businesses and new business models that eventually emerge. This all suggests that we won’t see the full effects of this wave of AI anytime soon.”

It’s fair to say that anyone who hazards a forecast of the impact and timing of AI on productivity and GDP growth is peering into a dense fog. As with every major technological innovation, the early forecasts tend to extrapolate the recent past and miss entirely the most significant ultimate impacts. Who could have predicted in 1900 that the automobile (dubbed the horseless carriage) would utterly transform the landscape, the economy and the culture; or who foresaw in the mid-1980s, when the internet was largely used for communication among small cadres of academics, that it would universalize access to information, spawn social media and upend entire sectors of the economy; or that the plain old telephone would morph into a powerful computer in everybody’s pocket.

That said, we can infer from the earlier summary list of examples how AI is likely to overcome the various “headwinds” that have caused the rate of productivity growth in advanced economies to trend down since the early 1970s:

- AI clearly has the potential to transform productivity in most aspects of the service sector, just as earlier generations of machinery and factory automation did in agriculture and manufacturing. A services-focused economy will eventually no longer be a brake on robust productivity growth;

- Through its potentially transformative impact on education and training, AI promises to generate a new era of growth in average skills and competencies (human capital), possibly analogous in productivity impact to universal grade-school and widespread post-secondary education; and

- The greatest productivity impetus of AI would come from its impact on the rate of innovation itself through augmentation of the human processes of discovery, understanding and invention. Here the crystal ball is especially hazy, but the potential implications are most profound.

This vision is unabashedly optimistic. In purely technological terms, it is plausible, although the path forward is sure to be strewn with conceptual and engineering obstacles. Meanwhile, the reality of the AI transformation will be tempered by culture and politics and by the social habits and vested interests that constitute the status quo. Change is never easy. Change of the magnitude projected from the examples above will be disruptive, as has been the case with every major technological revolution. But opting out is not an option.

Every major new technology carries society on a voyage into the unknown, buoyed by imagined benefits but always bringing risks. This inevitably creates a tension between innovation and restraint. Government finds itself on both sides seeking to maximize the opportunities while minimizing the risks. Artificial intelligence, more than any preceding technology, presents the greatest challenge of managing the opportunity-risk tension because of the scope and scale of its impact, the sheer pace of innovation, the largely opaque nature of the technology itself, and its inherently borderless characteristics.

There has been a great deal of discussion of the foreseeable as well as the potential risks of AI, from the relatively mundane to the existential.[42] Figure 7 shows there is widespread public concern regarding a range of anticipated impacts of AI. Canadians appear to be among the most worried, ranking at or above a 21-country average on almost every impact area. This is to be expected given the widely cited concerns expressed[43] by some prominent Canadian AI experts together with a natural wariness of the unknown, particularly given experience with the downsides of social media and rampant disinformation online. Moreover, most of the potentially positive and compelling applications of AI have yet to appear.

Figure 7

Source: Data for the countries shown in the table are from the graphic on page 17 of Chapter 9 of the 2024 AI Index Report. The countries were selected by the author.

The focus of this paper is on those positive applications and specifically on the economic significance of AI. But unless public skepticism is credibly addressed by governments and businesses, many beneficial applications of AI will be delayed or prevented. And so, too, would be the positive impact on Canada’s productivity and living standards. That’s why the positive case for AI needs to be complemented by compelling evidence that the understandable public concerns can be effectively managed.[44]

While it is beyond the scope of this discussion to address all aspects of the public anxiety regarding AI, there are three issues directly associated with the economic implications that have seized the attention of policymakers everywhere. They are:

- The impact of AI on employment;

- Assuring healthy competition in the AI marketplace; and

- Regulating the role of AI in provision of goods and services.

Experience from past technological revolutions suggests that each can be managed so that AI’s transformative benefits are achieved while preserving human values and purpose.

As described earlier, AI (or any other productive technology) increases labour productivity by automating certain tasks, and/or by augmenting the capabilities of a human worker. In either case, more output is produced per human hour worked. The extra value created shows up as increased compensation for workers and/or owners of AI capital. This increases overall demand in the economy, a portion of which generates new work for humans, including potentially for those initially replaced by AI.

The ultimate impacts on employment and on the shares of new income going to labour and to capital are complex and hard to foresee precisely. But the history of technological change demonstrates unequivocally that technology does not kill jobs overall; technology simply changes what jobs get done. For example, in the first decade of the 20th century, a million Canadians — about 35 percent of the entire workforce — were employed in farming. In 1970, the number had fallen to 480,000 or 5.6 percent of total employment. By 2023, agricultural employment was down to 256,000, a mere 1.3 percent of Canadian jobs. But total farm output was many times greater than 50 or 100 years earlier. That’s the payoff from productivity growth. Meanwhile, the farm employment displaced by agricultural machinery and crop science was replaced by new jobs in rapidly expanding manufacturing and service industries.

By 1975, manufacturing accounted for about 20 percent of Canadian employment[45] and services for 65 percent. Then, as technology enabled rapid productivity growth in manufacturing, that sector’s employment share fell from 20 percent to nine percent currently, while employment shifted into an expanding range of services that now account for 80 percent of Canadian jobs. And within the broad ambit of services, there continues to be dynamic birth and death of job categories — very few clerk-typists but lots of marketing managers, for instance.

People nevertheless focus on the particular job that is lost. It’s tangible and attached to a human face and to a community. The offsetting job that will eventually be created is an abstraction and may or may not be there for any particular individual. But new, unimagined jobs always do appear. A recent study[46] in the U.S. showed that 60 percent of employment in 2018 was in job titles that did not exist in 1940.

So, in terms of impact on total employment, AI will be no different from past technological changes. Some jobs will disappear; new jobs will be created; and the resulting productivity growth will cause society’s material standard of living to increase. But the impact will vary according to the sector of the economy, the specific job functions (“tasks”) that AI either automates or augments, and the characteristics of the impacted workforce — for example, education, age, gender and income.

A recent study[47] published by the Canadian Chamber of Commerce shows which industries are most and least likely to be affected by AI in the near term (see Figure 8). Not surprisingly, the sectors most exposed to generative AI applications are those that mainly produce and use information, and the least exposed are those that engage heavily with the physical world or provide services that employ the human touch, like health care and social assistance.

Nevertheless, within every sector there are always specific tasks that can be automated or augmented by AI — such as administrative and decision-making support, document preparation, data analysis or any task that requires subtle pattern recognition. In any event, AI is most likely to augment higher-skill jobs and automate those with lower-skill requirements. That effect would be to increase income inequality. On the other hand, in the case of AI augmentation, the benefit appears to be greatest for less experienced employees,[48] presumably because the present generation of AI provides a smaller advantage to the most expert.

Figure 8

Source: The graphic is taken directly from page 17 of this report.

What can be said with confidence is that even as AI capability increases, there will still be things for humans to do, and the productivity growth enabled by AI will create a larger economic pie to be shared. The policy issue[49] is therefore to manage the transition and to ensure that the new value generated by AI is shared fairly. These are not new challenges. In the context of past technological revolutions, they have been met, for example, with innovations in public policy such as universal education, progressive taxation, various worker protections, re-training and the broad range of social programs that constitute the welfare state. Looking forward, we can build directly on that experience and innovate to address what will be unprecedented about the AI transition. The lesson is that it’s society’s choice as to how the employment impact of AI will be managed.

Creation of a state-of-the-art AI is hugely expensive due to the top-end processors (GPUs) and data centre resources required: training Google’s “Gemini Ultra” model in 2023, for instance, is estimated to have cost almost US$200 million.[50] A small number of transnational giants dominate the field — led by Microsoft, Google, Amazon and Meta — that possess the human talent, cloud infrastructure, access to massive proprietary data sets and customer channels, as well as the financial muscle to stay in the game. These companies can afford the “entry fee,” after which provision of the resulting AI services is comparatively low-cost. A very significant barrier faces prospective competitors.

Vigorous competition is obviously beneficial for users and promotes the innovation that drives an emerging field like AI. Moreover, excessive concentration of private influence over a strategically vital technology like AI can threaten the public interest, including national security. Nevertheless, financial scale and private sector creativity are essential at this stage of the evolution of AI. So, a delicate regulatory balance must be struck.

Fortunately, policies that promote fair and competitive markets have a long history that can be readily applied to the AI domain, such as review of merger and acquisition deals and anti-trust regulation. Beyond that, recent experience with respect to the information and communications technology sectors will be of direct relevance in promoting a competitive environment. For example:

- Non-discriminatory access to cloud resources and other data infrastructure will be essential. Rules in an AI context could draw on experience in ensuring fair access to telecommunications networks;

- Choke points resulting from proprietary control of the most powerful AI models can be mitigated by support of open-source platforms like Hugging Face[51] and EleutherAI.[52] There is a very large global community of researchers, developers and financiers prepared to volunteer skill, time and money to ensure a rich ecosystem of AI models analogous to those that developed open-source computer operating systems like Linux; and

- Competitive AI development depends on affordable access to enormous computing power. Governments can contribute, as they have in the past, to this infrastructure. For instance, the federal government has earmarked[53] $2 billion over five years to launch a new AI compute access fund and a Canadian AI sovereign compute strategy.

These examples illustrate the rich body of already-established regulation and practice that can promote a competitive AI ecosystem. What is nevertheless a unique challenge is to ensure fair access to the enormous volumes of data on which AI models are trained. Data is the fuel that powers generative AI and access to it has emerged[54] as a contentious and potentially limiting constraint on future development. Policy creativity will be required to establish protocols for responsible data sharing that allow smaller companies to access high-quality datasets while maintaining user privacy, and to ensure that users and businesses have control over their data and can port it between platforms, enabling them to move from one AI service to another.

The sale and use of “products” — whether tangible goods or services — is already subject to extensive regulation regarding safety, liability, transparency, privacy, non-discrimination and consumer protection, among other things. How might this existing framework be adapted to the inclusion of AI? In many cases, it’s relatively straightforward to apply existing regulations/standards. For example, product liability laws can be extended to AI-enhanced goods (e.g., medical devices), as can consumer protection regulations (e.g., to guard against deceptive practices), and anti-discrimination laws (e.g., to remove bias in AI-enhanced credit scoring or job screening). Professional licensing standards can be adapted to cover situations where AI is “included in the loop” through proof of competency — for instance, use of an AI in radiology[55] should first have to conclusively demonstrate competency at least equal to the human standard.

While a great deal of product regulation can be simply “ported” into an AI environment with minimal adjustment, there are unique features of the technology that call for regulatory creativity. For example, generative AI is a dynamic, evolving learning mechanism that is in effect a “black box” with an opaque reasoning process that may inherit potential biases lurking in its training data or provide false answers. These characteristics create unique challenges in establishing the trustworthiness of AI products, particularly in important applications such as health care, legal contexts, autonomous driving and financial decision-making.

It’s obviously in the provider’s interest to prove to users that its products are safe and perform as promised. That’s why a lot of technical effort is being made to minimize “hallucinations,” to improve the “explainability” of AI’s decisions and generally to improve the amount and quality of training data for particular application domains. That motivation coming from the market can be amplified by application of existing regulations regarding liability and consumer protection, as noted above. Crucially important in the latter regard is to require explicit notification when AI is a significant component of a product.[56]

Ultimately, the way to prove performance and establish trust in AI products is through disciplined demonstration of safety and efficacy. The required rigour would vary depending on the importance of the application. A lot of AI products should be “regulated” simply by market acceptance or rejection. But where more is at stake, rigorous testing protocols need to be developed and enforced. A number of methods have been applied or proposed, including, for example: “red teaming,” which involves stress tests on AI systems to identify vulnerabilities and weaknesses; independent audits of an AI system’s performance, safety and compliance with ethical standards; “regulatory sandboxes”[57] in which an AI product would be tested in a tightly limited user environment and subject to light regulation; and controlled product testing (analogous to clinical trials for drug approval) as part of a certification process — like the millions of kilometres driven before autonomous vehicles are certified.

Meanwhile, a great deal of work is underway at both the national and international levels to develop principles and codes of conduct to govern the development and use of advanced AI systems.[58] Given the inherently global nature of the AI phenomenon, it’s obviously important to achieve as much international commonality as possible to minimize opportunities for regulatory arbitrage and inconsistent compliance obligations on transnational companies. Notable in this regard is the Hiroshima AI Process[59] launched by the G7 in May 2023 to establish a framework for the trustworthy governance of AI systems. Although initiated by the G7, the framework invites international co-operation involving developing countries, private entities and academic institutions. The next stage in the development of the process will be a focus of Canada’s presidency of the G7 in 2025.

The national approaches to AI regulation in the U.S., EU, China and Canada are summarized in Box III. Together with transnational initiatives to achieve harmonization, a concerted global regulatory effort is underway to earn the trust of an often skeptical public. Inevitably, this will be an evolving learning process. But the history of managing past technological revolutions provides both the confidence that AI can be managed for human benefit and lessons as to how that can be accomplished.

National approaches to AI regulation

United States: The U.S. approach to AI policy focuses on promoting innovation while addressing potential risks through a combination of voluntary frameworks and sector-specific regulation. There is no comprehensive federal AI or privacy legislation, but an AI bill of rights provides non-binding executive guidelines. The White House 2023 executive order[60] on AI co-ordinates significant federal AI efforts, including mandatory safety testing for the most advanced systems.

European Union: The EU has been at the forefront of AI regulation. The AI Act[61] (2024) is the world’s most ambitious regulatory framework, classifying AI systems into risk categories with strict obligations on the highest risk systems. The act also bans certain AI practices entirely, such as deploying subliminal techniques to materially distort opinions in a democratic society. The act is expected to come into force in 2026 after a two-year grace period.

China: China has implemented several AI-related regulations, for example interim measures[62] for the administration of generative AI services that regulate AI-generated content and emphasize the need for safety and control over misinformation. But China has not yet passed a comprehensive law. Its approach is state-driven and employs strict regulations, particularly regarding the ethical use of AI, the protection of state interests, data privacy and technological self-reliance.

Canada: At the federal level, Canada has adopted a balanced approach, promoting innovation while working on legislation to regulate AI’s societal impact. The principal features to date are:

- The pending Artificial Intelligence and Data Act (AIDA),[63] which focuses on high-impact AI systems similar to the EU’s AI Act but leaving more room for regulatory flexibility;

- The directive on automated decision-making[64] is in place for federal government AI use;

- The Voluntary code of conduct[65] on the responsible development and management of advanced generative AI systems, launched in September 2023, and signed by major tech companies; and

- The 2017 pan-Canadian artificial intelligence strategy,[66] renewed in 2022. Canada is a founding member of the Global Partnership on Artificial Intelligence (GPAI),[67] a multi-stakeholder initiative that promotes the responsible development and use of AI.

Common features: Across all four regions, there is:

- A clear emphasis on developing AI in ways that respect human rights and ethics;

- Priority for oversight, transparency and accountability mechanisms to mitigate AI risks; and

- A policy framework that seeks to balance regulation with the need to foster AI innovation. The U.S. prioritizes innovation with a lighter regulatory touch, while China aims for global AI leadership through state-directed initiatives.

Divergent features: The EU and China are more proactive in setting comprehensive and binding regulations, while the U.S. and Canada are adopting more flexible, innovation-driven policies. Canada and the EU are actively involved in international forums like GPAI and the Hiroshima AI Process, aiming for global consensus on AI governance, whereas the U.S. tends to emphasize international leadership through technological dominance. China is more insular in its AI development, prioritizing national objectives, although it has engaged in some global AI dialogues.

Is Canada ready, willing and able to seize the AI opportunities outlined in this paper? The answer, at least in the author’s opinion, is a qualified “Yes.” We come to the AI revolution with several significant advantages:

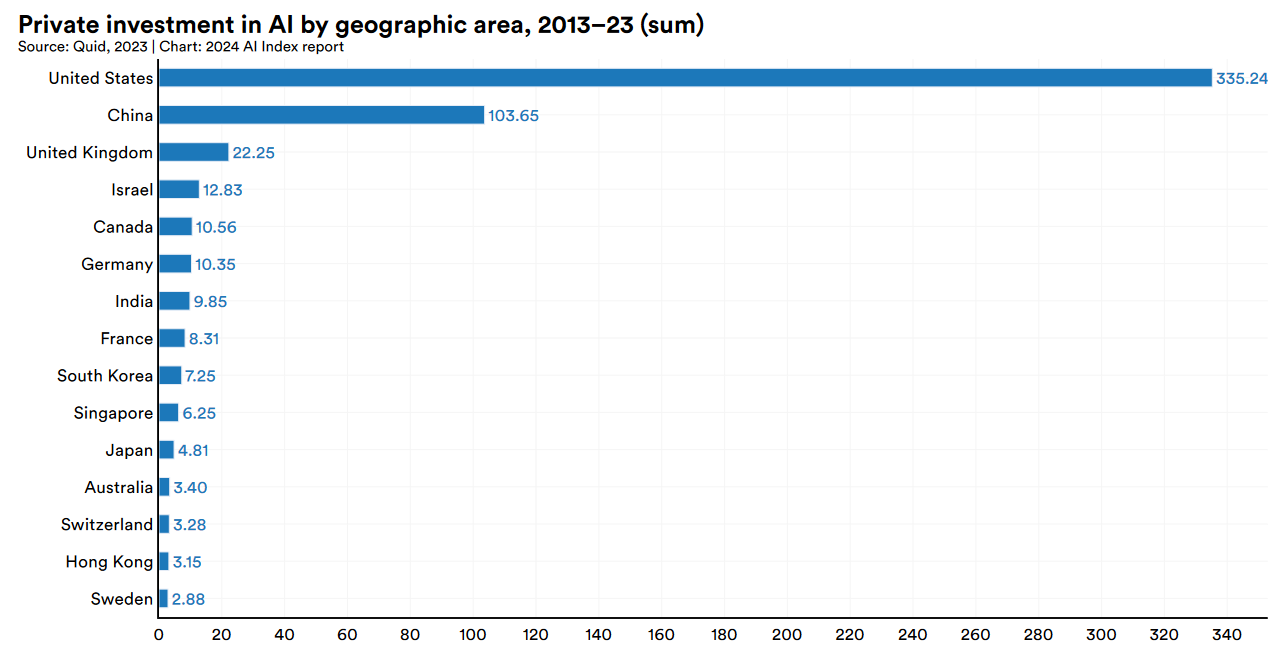

- Research excellence: Canada is home to genuinely world-class AI research capability with (a) global leaders in the field like Yoshua Bengio (co-recipient of the Turing Award, the most prestigious recognition in computer science), Geoffrey Hinton (Turing Award co-recipient and Nobel laureate), and Richard Sutton (internationally renowned for his pioneering work on “reinforcement learning”), among many others; and (b) three top-ranked national AI research organizations — Mila in Montreal, Vector Institute in Toronto and Amii in Edmonton — as well as vibrant regional hubs from coast to coast. This outstanding intellectual capital has branded Canada as a global leader while supporting a steady flow of superbly trained talent, thus making the country a compelling destination for investment. In the 10 years through 2023, Canada attracted almost US$11 billion of private investment in AI, the 5th largest total in the world, although only seven percent as much as the U.S., by far the global leader (see Figure 9).

Figure 9

Source: Figure is taken directly from page 36 of Chapter 4 of the 2024 AI Index Report.

- A base of globally competitive AI companies: Canada has already established a solid position in the still-emerging AI industry with pioneering companies like Kinaxis, Coveo, Element AI (since acquired by ServiceNow), BlueDot, Mindbridge and BenchSci, among many others. Cohere[68] — co-founded in 2019 by CEO Aidan Gomez, a member of the Google team that developed the transformer architecture — is recognized as a world leader in the integration of LLMs in various enterprise applications. Canada’s major banks are among the global leading developers and users of AI in finance, with RBC currently ranked 3rd and all of the Big Five ranked in the global Top 25, according to the Evident AI Index,[69] the gold standard rating institution for AI in banking.

- Supportive government: The federal government, early on, made AI a focus of support — beginning with the 2017 pan-Canadian AI strategy, managed by the Canadian Foundation for Advanced Research (CIFAR),[70] and so far funded with $567 million.[71] In addition, the 2024 federal budget included $2.4 billion for several AI support initiatives, headlined by $2 billion for computing power needed to train and operate Canadian-based AI models. Regarding AI regulation and governance, although the proposed Artificial Intelligence and Data Act has unfortunately been delayed in Parliament, the government has been active in various international forums, notably the G7 Hiroshima AI Process and the GPAI. Provincial governments have also been developing AI industrial strategies, most notably Quebec, which has pledged a $217 million investment in the AI sector[72] (2022-27).

Despite these impressive advantages, Canada continues to be challenged by the long-standing difficulty[73] of converting its leading-edge knowledge into commercial innovation. This is the legacy of Canada’s industrial structure — weighted toward resource extraction, construction, finance and U.S. branch plant investment — that reflects the country’s traditional position within a tightly integrated North American economy. The AI revolution creates the opportunity to turn the page. But this will depend on the willingness of businesses large and small and in virtually every sector of the economy to step up to the opportunity.

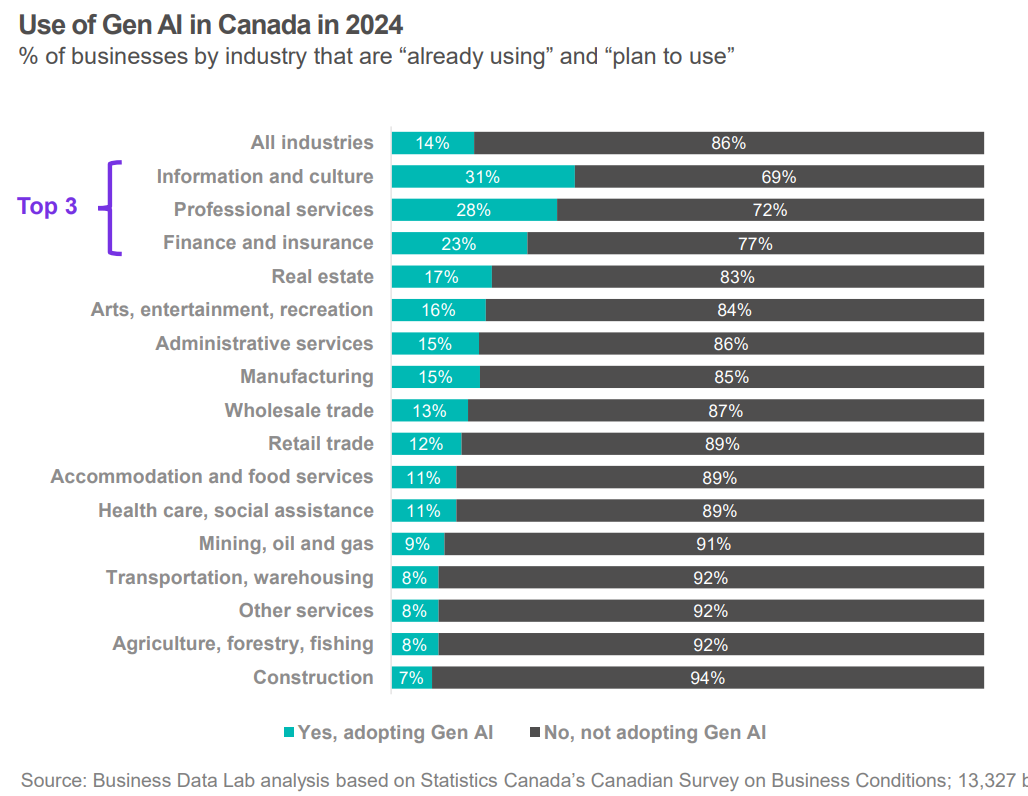

So far, the response has been mixed. While Canada is well represented, relative to the size of its economy, by companies that are creating advanced AI services, uptake of applications has so far been limited.[74] Polling of a representative sample of more than 13,000 businesses by Statistics Canada revealed[75] that only 14 percent have used generative AI tools or are imminently planning to do so, while almost three-quarters are not even considering the option.[76] They give a variety of reasons, such as no business case has been identified, they lack the skills, or they’re concerned about data privacy, cost and financing. While it’s still early days, the technology is moving very fast and users who embark early on the learning curve are much more likely to end up with a durable competitive advantage. Moreover, the impact of AI on Canada’s rate of productivity growth depends almost entirely on the extent and speed of uptake of applications by businesses and public sector entities.

It’s beyond the scope of this scene-setting paper to propose further specific policy measures to promote and accelerate the application of AI in Canada’s economy. That job will be the subject of future work by the Public Policy Forum. Following from the big-picture analysis in this paper, three theme areas should be the key elements of an AI industrial strategy for Canada:

- Regulatory development and harmonization: A lack of regulatory certainty is well-known to discourage investment and AI will be no exception. Given the extremely dynamic nature of the field, AI regulation will inevitably be in flux, but every effort needs to be made to formulate and adhere to basic principles and achieve consistency across jurisdictions. Canada acting alone has little influence on the course of AI governance and regulation, and therefore must continue to play a leading role in global forums like the Hiroshima AI Process and standards-setting bodies. Domestically, it is essential to promote AI regulatory harmonization in areas of shared jurisdiction and among provinces in their areas of exclusive jurisdiction, such as delivery of health care, education, energy and resource development. Rules in respect to data and privacy are central to development and use of AI models and thus require priority attention. Because AI creates many unprecedented opportunities and issues, domestic collaboration and harmonization may be easier to achieve than has been the case for established regulatory domains.

- Supporting high pay-off sectors: An AI industrial strategy requires that choices be made. While this is tough to do in a geographically and culturally vast federation like Canada, our resources are limited and impact depends on their focus. For example, the world is undergoing a multi-decade transformation of the energy system to renewably generated electricity. AI can play a major role[77] in this historic transition, but market forces alone in the heavily regulated electricity sector may not be sufficient to seize the opportunity in a timely way. Well-designed policy and program interventions can tip the balance. Beyond that, there is a limited number of areas that have particular potential to boost productivity through application of AI due either to their scale and importance or their strategic position in the economy, such as health-care systems and supply-chain logistics. Government support should be directed preferentially to such high-impact areas.

- Government as a model user of AI: The ancient proverb “physician, heal thyself” applies. There are at least three ways by which the application of AI to the government’s own operations can make a major contribution to an AI-based industrial strategy:

- AI applied in the administrative and decision-support functions of government promises eventually to improve the efficiency and quality of service. If well-delivered, this will increase public confidence in AI applications, without which AI’s potential to improve productivity will be greatly diminished;

- A government committed to AI can be a lead customer for Canadian suppliers through strategic procurement. The government, as an early buyer, can help suppliers ascend the learning curve and then provide the validation that promotes market expansion. But this approach cannot work without explicit acknowledgement from the top that it’s an element of industrial strategy and consequently requires extra time and cost; and

- Finally, a government’s committed use of AI will provide a wealth of practical experience from a user’s perspective to inform development of wise policy and regulation in this novel area.

While artificial intelligence is still in its infancy, the child is already precocious. With the sudden advent of generative AI, the revolutionary potential of AI for human betterment has become evident. Because AI amplifies — and in many ways mimics — the human mind, it has no precedent in the history of technology. With great power also comes great risk. But the risk has to be accepted and managed because AI cannot be “unlearned,” nor can its development be terminated for the simple reasons that the prospective benefits are so compelling and there’s no jurisdiction on Earth that has the authority and power to call a halt.

Will AI power a new era of productivity growth and material prosperity in Canada? Yes, it will. Only the precise trajectory, and especially the timing, remain to be discovered.

Endnotes

- Canada’s per capita GDP in 2023 was $58,840 (2017 dollars), compared with $56,610 in 2013, implying an annual average growth rate of merely 0.4 percent. In fact, GDP per capita was lower in 2023 than five years earlier in 2018: McCormack, C., and Wang, W. (Apr. 24, 2024). Canada’s gross domestic product per capita: Perspectives on the return to trend. Statistics Canada. https://www150.statcan.gc.ca/n1/pub/36-28-0001/2024004/article/00001-eng.htm. ↑

- Bergeaud, A., Cette, G., and Lecat, R. (n.d.). Long-Term Productivity Database. Bank of France. http://www.longtermproductivity.com/. ↑

- Per capita GDP is by definition “GDP/worker X workers/population” or productivity multiplied by employment as a percent of the population (the “employment ratio”). The annual growth rate of GDP per capita is equal to the growth rate of productivity plus the growth rate of the employment ratio. As the population ages, the latter ratio tends to decline and per capita GDP growth comes to depend entirely on productivity growth. That’s where we are today. ↑

- Stanford economist Charles Jones and co-authors have shown that new ideas have been getting harder to find. Research efficiency — defined as productivity growth per researcher — has declined steadily even as R&D effort has increased rapidly: Jones, C., et al. (2020). Are Ideas Getting Harder to Find? American Economic Review 110(4): 1104–1144. https://web.stanford.edu/~chadj/IdeaPF.pdf.Economic historian Robert Gordon has also argued persuasively that the innovations associated with information technology have, so far, failed to drive productivity increases comparable to those of the past hundred years: Gordon, R. (August 2012). Is U.S. Economic Growth Over? Faltering Innovation Confronts the Six Headwinds. National Bureau of Economic Research. https://www.nber.org/papers/w18315. ↑

- Imagine that a quantity like productivity (output per hour), starting at 100, is growing at three percent. The first year it grows by three units to 103. By the 25th year (1.03^25) it has grown to 209 units. To continue to grow three percent in the 26th year requires a new increment of 6.3 units — more than double the growth increment 25 years earlier. Eventually, new and better ways need to be found to maintain a steady annual growth rate. ↑

- Mokyr, J. (2006). Economic Transformations: General Purpose Technologies and Long-term Economic Growth. EH.NET. https://eh.net/book_reviews/economic-transformations-general-purpose-technologies-and-long-term-economic-growth/. ↑

- Sprague, S. (April 2021). The U.S. productivity slowdown: an economy-wide and industry-level analysis. Monthly Labor Review, U.S. Bureau of Labor Statistics. https://www.bls.gov/opub/mlr/2021/article/the-us-productivity-slowdown-the-economy-wide-and-industry-level-analysis.htm. ↑

- AI is not restricted to augmenting or substituting for existing human work. It will also increasingly create entirely new sources of value that are wholly beyond human capability; familiar examples are GPS navigation and web search engines. ↑

- Wikipedia. (Nov. 26, 2024.). Generative artificial intelligence. https://en.wikipedia.org/wiki/Generative_artificial_intelligence. ↑

- Open AI. (Sept. 12, 2024). Introducing OpenAI o1-preview. https://openai.com/index/introducing-openai-o1-preview/. ↑

- Strickland, E. (Feb. 14, 2024). What Is Generative AI? Spectrum explains large language models, the transformer architecture, and how it all works. IEEE Spectrum. https://spectrum.ieee.org/what-is-generative-ai. ↑

- NVIDIA. (June 2021). NVIDIA A100 Tensor Core GPU: Unprecedented Acceleration at Every Scale. NVIDIA Date Sheet. https://www.nvidia.com/content/dam/en-zz/Solutions/Data-Center/a100/pdf/nvidia-a100-datasheet-us-nvidia-1758950-r4-web.pdf. ↑

- McCullum, N. (June 28, 2020). Deep Learning Neural Networks Explained in Plain English. freeCodeCamp. https://www.freecodecamp.org/news/deep-learning-neural-networks-explained-in-plain-english/. ↑

- Murgia, M. et al. (Sept. 12, 2023). Generative AI exists because of the transformer. Financial Times. https://ig.ft.com/generative-ai/. ↑

- Roose, K. (Feb. 16, 2023). A Conversation With Bing’s Chatbot Left Me Deeply Unsettled. New York Times. https://www.nytimes.com/2023/02/16/technology/bing-chatbot-microsoft-chatgpt.html. ↑

- Vincent, J. (Feb. 16, 2024). How much electricity does AI consume? The Verge. https://www.theverge.com/24066646/ai-electricity-energy-watts-generative-consumption. ↑

- Penn, I., and Weise, K. (Oct. 16, 2024). Hungry for Energy, Amazon, Google and Microsoft Turn to Nuclear Power. New York Times. https://www.nytimes.com/2024/10/16/business/energy-environment/amazon-google-microsoft-nuclear-energy.html. ↑

- Open AI. (Sept. 12, 2024). Introducing OpenAI o1-preview. https://openai.com/index/introducing-openai-o1-preview/. ↑

- Stanford University. 2024. Artificial Intelligence Index Report 2024 — Chapter 4: Economy. https://aiindex.stanford.edu/wp-content/uploads/2024/04/HAI_AI-Index-Report-2024_Chapter4.pdf. ↑

- Goldman Sachs Exchanges. (June 27, 2024). Gen AI: too much spend, too little benefit? https://www.goldmansachs.com/insights/top-of-mind/gen-ai-too-much-spend-too-little-benefit. ↑

- The productivity growth impact of any innovation depends both on its “unit impact” and on the pace and extent of uptake. While many AIs have remarkable capabilities, their effect on economic growth will remain limited until they are widely deployed in commercial applications. ↑

- Peng, S., Kalliamvakou, E., Cihon, P., and Demirer, M. (Feb. 13, 2023). The Impact of AI on Developer Productivity: Evidence from GitHub Copilot. arXivLabs. https://arxiv.org/pdf/2302.06590. ↑

- Unknown author. (Apr. 9, 2024). Taking AI to the next level in manufacturing: Reducing data, talent, and organizational barriers to achieve scale. MIT Technology Review. https://www.technologyreview.com/2024/04/09/1090880/taking-ai-to-the-next-level-in-manufacturing/. ↑

- Harkness, L., Robinson, K., Stein, E. and Wu, W. (Dec. 5, 2023). How generative AI can boost consumer marketing. McKinsey & Company. https://www.mckinsey.com/capabilities/growth-marketing-and-sales/our-insights/how-generative-ai-can-boost-consumer-marketing. ↑

- Mohamed, Y., Khanan, A., Bashir, M., and Mohamed, A.H. (Feb. 23, 2024). The Impact of Artificial Intelligence on Language Translation: A Review. IEEE Access. https://www.researchgate.net/publication/378284156_The_Impact_of_Artificial_Intelligence_on_Language_Translation_A_review. ↑

- Maple, C., Szpruch, L., Epiphaniou, G., Staykova, K., et al. (August 2023). The AI Revolution: Opportunities and Challenges for the Finance Sector. ResearchGate. https://www.researchgate.net/publication/373552066_The_AI_Revolution_Opportunities_and_Challenges_for_the_Finance_Sector. ↑

- Wang., S., et al. (Oct. 15, 2024). Artificial intelligence in education: A systematic literature review. Expert Systems with Applications, 252(Part A). ScienceDirect. https://www.sciencedirect.com/science/article/pii/S0957417424010339. ↑

- Al-Hague, S., B-Lajoie, M., Eizenman, E., and Milinkovich, N. (Feb. 26, 2024). The potential benefits of AI for healthcare in Canada. McKinsey & Company. https://www.mckinsey.com/industries/healthcare/our-insights/the-potential-benefits-of-ai-for-healthcare-in-canada. ↑

- OECD. (June 13, 2024). Governing with Artificial Intelligence: Are governments ready? https://www.oecd.org/en/publications/2024/06/governing-with-artificial-intelligence_f0e316f5.html. ↑

- Google DeepMind. (Sept. 12, 2024). Our latest advances in robot dexterity. https://deepmind.google/discover/blog/advances-in-robot-dexterity/. ↑

- The Royal Society. (May 2024). Science in the age of AI. https://royalsociety.org/news-resources/projects/science-in-the-age-of-ai/. ↑

- Roser, M. (Feb. 7, 2023). AI timelines: What do experts in artificial intelligence expect for the future? Our World in Data. https://ourworldindata.org/ai-timelines. ↑

- Korosec, K. (Aug. 20, 2024). Waymo is now giving 100,000 robotaxi rides a week. Yahoo News. https://news.yahoo.com/news/waymo-now-giving-100-000-153212329.html?fr=yhssrp_catchall. ↑

- Lee, T.B. (Sept. 13,2024). 15 self-driving companies to watch. Understanding AI. https://www.understandingai.org/p/15-self-driving-companies-to-watch. ↑

- Waabi. (Mar. 18, 2024). Waabi to Bring the First Generative AI-Powered Trucking Solution, Built on NVIDIA DRIVE Thor, to Market. https://waabi.ai/nvidia-drivethor/. ↑

- Lee, T.B. (Sept. 11, 2024). How transformer-based networks are improving self-driving software. Understanding AI. https://www.understandingai.org/p/how-transformer-based-networks-are. ↑

- OECD. (Apr. 16, 2024). The impact of Artificial Intelligence on productivity, distribution and growth: Key mechanisms, initial evidence and policy challenges. https://www.oecd.org/en/publications/the-impact-of-artificial-intelligence-on-productivity-distribution-and-growth_8d900037-en.html. ↑

- Briggs, J., et al. (Mar. 26, 2023). Global Economics Analyst: The Potentially Large Effects of Artificial Intelligence on Economic Growth. Goldman Sachs. https://www.gspublishing.com/content/research/en/reports/2023/03/27/d64e052b-0f6e-45d7-967b-d7be35fabd16.html. ↑

- Billy-Ochieng, R., Arif, A., Garcia, D. (May 28, 2024). Artificial Intelligence Technologies Can Help Address Canada’s Productivity Slump. TD Economics. https://economics.td.com/ca-AI-tech-can-help-productivity-slump. ↑

- Nathan, A. (June 25, 2024). Gen AI: too much spend, too little benefit? Top of Mind, 129. Goldman Sachs. https://www.goldmansachs.com/images/migrated/insights/pages/gs-research/gen-ai–too-much-spend%2C-too-little-benefit-/TOM_AI 2.0_ForRedaction.pdf. ↑

- Macklem, T. (Speech on Sept. 20, 2024). Artificial intelligence, the economy and central banking. Bank of Canada. https://www.bankofcanada.ca/2024/09/artificial-intelligence-the-economy-and-central-banking/. ↑

- Roose, K. (May 30, 2023). A.I. Poses ‘Risk of Extinction,’ Industry Leaders Warn. New York Times. https://www.nytimes.com/2023/05/30/technology/ai-threat-warning.html. ↑

- Isai, V. (May 27, 2023). Canada Needs to Hurry on A.I. Oversight, Experts Warn. New York Times.https://www.nytimes.com/2023/05/27/world/canada/chatgpt-canada-ai-oversight.html. ↑

- A recent study for the Canadian Chamber of Commerce underscored the point noting that “the factor of “trust” will be important for future adoption, with public interest and acceptance of AI likely being positively correlated with countries’ business adoption rates:” Gill, P. (May 22, 2024). Business Data Lab Report Projects Gen AI Tipping Point for Businesses. Canadian Chamber of Commerce. https://chamber.ca/news/business-data-lab-report-projects-gen-ai-tipping-point-for-businesses-faster-adoption-needed-to-rescue-canada-from-its-productivity-emergency/. ↑

- Statistics Canada. (Jan. 5, 2024). Labour force characteristics by industry, annual (x 1,000). Government of Canada. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1410002301. ↑

- Autor, D., et al. (2024). New Frontiers: The Origins and Content of New Work, 1940-2018. The Quarterly Journal of Economics, 139(3). Oxford University Press. https://blueprintcdn.com/wp-content/uploads/2024/07/new_frontiers_the_origins_and_contents_of_new_work_1940-2018_autor_chin_alomons_seegmiller.pdf. ↑

- Gill, P., and DiCapua, A. (May 30, 2024). Prompting Productivity: Generative AI Adoption by Canadian Businesses. Canadian Chamber of Commerce. https://businessdatalab.ca/wp-content/uploads/2024/05/Prompting_Productivity_Report_May30_2024.pdf. ↑

- Brynjolfsson, E., Li, D., and Raymond, L.R. (November 2023). Generative AI at Work. Stanford Graduate School of Business. https://www.gsb.stanford.edu/faculty-research/working-papers/generative-ai-work. ↑

- Cazzaniga, M., et al. (Jan. 14, 2024). Gen-AI: Artificial Intelligence and the Future of Work. International Monetary Fund. https://www.imf.org/en/Publications/Staff-Discussion-Notes/Issues/2024/01/14/Gen-AI-Artificial-Intelligence-and-the-Future-of-Work-542379. ↑

- Global private investment in AI in 2023 was almost $100 billion. The U.S. dominates with almost 70 percent of the total, far ahead of China’s eight percent and Canada’s 1.7 percent: Unknown author. (2024). The AI Index Report: Measuring trends in AI. Stanford University. https://aiindex.stanford.edu/report/#individual-chapters. ↑

- Hugging Face. (n.d.). About: The AI community building the future. https://huggingface.co/. ↑

- EleutherAI. (n.d.). About: Empowering Open-Source Artificial Intelligence Research. https://www.eleuther.ai/. ↑

- Innovation, Science and Economic Development Canada. (June 26, 2024). Government of Canada launches public consultation on artificial intelligence computing infrastructure. Government of Canada. https://www.canada.ca/en/innovation-science-economic-development/news/2024/06/government-of-canada-launches-public-consultation-on-artificial-intelligence-computing-infrastructure.html. ↑

- Roose, K. (July 19, 2024). The Data That Powers A.I. Is Disappearing Fast. New York Times. https://www.nytimes.com/2024/07/19/technology/ai-data-restrictions.html. ↑

- Hillis, J.M. et al. (Mar. 15, 2024). The lucent yet opaque challenge of regulating artificial intelligence in radiology. npj Digital Medicine. Springer Nature Group. https://www.nature.com/articles/s41746-024-01071-2. ↑

- A requirement for AI transparency is needed to minimize deceptive practices such as the use of “deep fakes,” AIs masquerading as humans, personal targeting based on facial recognition, etc. Effective control of these practices will depend on technological countermeasures combined with legal sanctions proportionate to the risk of harm. ↑

- Madiega, T.A. (June 17, 2022). Artificial intelligence act and regulatory sandboxes. European Parliament Think Tank. https://www.europarl.europa.eu/thinktank/en/document/EPRS_BRI(2022)733544 ↑

- Significant initiatives include: OECD AI Principles; G7 Hiroshima AI Process; UNESCO Recommendation on the Ethics of AI; Global Partnership on AI (involving governments, industry and academia); ISO/IEC AI Standards; EU Artificial Intelligence Act; and the U.S. AI Risk Management Framework (developed in 2023 by the National Institute of Standards and Technology). ↑

- Hiroshima AI Process. (2023) Documents of Achievement. https://www.soumu.go.jp/hiroshimaaiprocess/en/documents.html. ↑

- White House. (Oct. 30, 2023) FACT SHEET: President Biden Issues Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. U.S. government. https://www.whitehouse.gov/briefing-room/statements-releases/2023/10/30/fact-sheet-president-biden-issues-executive-order-on-safe-secure-and-trustworthy-artificial-intelligence/. ↑

- European Parliament. (June 18, 2024). EU AI Act: first regulation on artificial intelligence. https://www.europarl.europa.eu/topics/en/article/20230601STO93804/eu-ai-act-first-regulation-on-artificial-intelligence. ↑

- Wu, Y. (July 27, 2023). How to Interpret China’s First Effort to Regulate Generative AI Measures. China Briefing. https://www.china-briefing.com/news/how-to-interpret-chinas-first-effort-to-regulate-generative-ai-measures. ↑